Comar recently sponsored a webinar focused on Driving Change in Diagnostics: Market Trends and Technological Advances. Moderated by Sean Pensky, Editor at Medical Product Outsourcing, the webinar featured Tony Freeman, President of A.S. Freeman Advisors, a transaction advisory and strategic consulting firm providing services to firms in the manufacturing industry.

Freeman explored the powerful shifts taking place in the diagnostics industry and examined how the diagnostics space is reacting differently to market shifts and changes than the rest of the healthcare industry. He presented an in-depth analysis of current trends in diagnostics, examining the economic and technological forces shaping the future of in vitro diagnostics (IVD).

Faced with rapidly rising healthcare costs and a shifting patient demographic, diagnostics is poised for a transformation. Freeman suggested that by extending diagnostics into patient hands, the industry can help curb rising healthcare costs while improving overall patient outcomes.

Key changes in technology and market demands are moving diagnostics from large, centralized labs to more accessible, consumer-focused devices and tests, ultimately pushing diagnostics more into homes and everyday healthcare settings. Below, you will find a closer look at the key points from the discussion, along with the embedded video so you can catch up quickly through our summary or watch the video in its entirety.

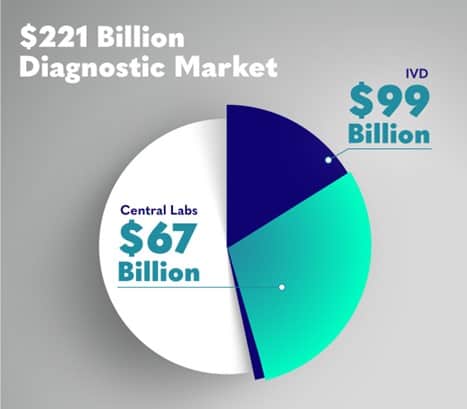

The diagnostics market is seeing remarkable growth and is projected to reach $221 billion US (specifically related to OEM dollars). This is the projected amount OEMs will invoice for this year. As the largest single segment in this market, in vitro diagnostics (IVD) represents nearly half of this number at $99 billion.

In recent years, demand for diagnostics solutions has been amplified by technological advances, enabling faster, more accessible testing options for both medical professionals and patients. IVD solutions are used extensively across healthcare due to their effectiveness in identifying diseases early and monitoring ongoing conditions.

Market Segmentation and Growth: Diagnostics is divided into subsegments, including central lab and point-of-care (POC) solutions. These segments are evolving, driven by a compound annual growth rate (CAGR) of 5.8% projected through 2030, which is slightly higher than the wider med tech market. Notably, POC testing, which includes both clinic- and home-based diagnostics, is emerging as a critical growth driver, allowing patients quicker access to essential health information.

Focus on In Vitro Diagnostics: IVD comprises the largest segment within diagnostics, valued at $99 billion, with notable advancements in POC solutions. Shifting from solely laboratory-based equipment, IVD is expanding into devices patients can use directly at home or at local clinics, bridging a critical accessibility gap. The “central labs,” comprised of the larger labs like Quest Diagnostics and LabCorp, dominate with the largest share of the $99 billion, grabbing around $67 billion of that segment of the market.

A primary driver of the diagnostics industry’s evolution is the unsustainable nature of current healthcare costs. With healthcare expenditures consuming up to 18% of GDP in developed nations, there’s an increasing need to detect diseases early to reduce long-term treatment costs. The aging global population compounds this urgency, as healthcare needs grow with age.

The economic strain is only expected to intensify as the global population ages. The number of people over 60 years old is projected to nearly double from 12% in 2020 to approximately 22% in 2050, potentially adding millions to healthcare systems that are already stretched thin. In 2020, there were more people over 60 in the US than there were under 5 years old for the first time in human history. These types of changes are contributing to the rise in spending on healthcare in the US and across the world. In the United States alone, healthcare costs make up 17.8% of GDP—a trend expected to rise. Early detection of diseases such as cancer, diabetes, and stroke could significantly curb these costs.

Cost-Saving Potential of Early Diagnostics: Freeman shared specific examples of how diagnostics can drastically reduce treatment costs. For example, prostate cancer testing costs between $20 to $50 but saves approximately $3,000 per patient over five years by enabling early treatment. Similarly, the cost of a C-reactive protein test, an early indicator of ischemic stroke, is about $20. Whereas, treating a stroke, one of the most expensive conditions to treat in medicine, costs roughly $125,000 in the first year alone, with a significant portion of that cost then recurring year-over-year. Such early tests represent a high-value, low-cost solution, one that insurance companies are likely to back in the future.

By lowering costs and improving outcomes, early diagnostics hold promise for reshaping healthcare economics and creating a sustainable model.

To meet the demand for early detection, diagnostics must move beyond centralized lab settings and into accessible locations such as clinics, pharmacies, and homes. This shift requires innovation in product design and development to ensure reliability and accuracy across varied environments. Freeman explained how this shift from the lab to the consumer will bring unique manufacturing and packaging challenges.

The shift toward point-of-care and at-home diagnostics brings new requirements for the diagnostics supply chain. Unlike centralized labs that rely on large machines and controlled environments, consumer-oriented diagnostics need to be robust, reliable, and straightforward for use in varied conditions. This shift calls for specialized expertise that diagnostic companies may need to source externally.

These changes will likely prompt diagnostic companies to form new partnerships and bring supply chain experts into the product development process early to ensure that diagnostic products are both user-friendly and effective outside the laboratory.

In closing, Freeman made a compelling case for the shift toward early, accessible diagnostics as both a healthcare and economic imperative. With healthcare costs rising unsustainably, the industry must innovate to bring diagnostics to the patient rather than relying on traditional lab settings. This transformation, however, requires not just technological innovation but also an overhaul of the supply chain to support consumer-oriented diagnostics.

As diagnostics become a consumer staple, similar to over-the-counter medications, public health outcomes could see dramatic improvements. Insurance companies and national health organizations, incentivized by the lower costs of early detection, are likely to support a push for expanded diagnostics accessibility. Government policy is another factor that could play a role in encouraging diagnostics at an earlier stage to alleviate future healthcare spending.

Freeman’s insights underscore the future of diagnostics as one where patient-centered, accessible testing becomes the standard. This transition will not only transform healthcare economics but also empower individuals to take control of their health through early detection and intervention.

The diagnostics industry stands on the brink of a new era. With technology advancing and economic needs pressing, the push for accessible diagnostics is gaining momentum. By decentralizing testing, leveraging supply chain innovation, and aligning with healthcare economics, diagnostics can become a vital part of proactive patient care.

As we move into this new era of med tech and diagnostics, Comar is uniquely positioned to support your needs with manufacturing solutions for diagnostics. We design solutions that work seamlessly with the required chemistry to ensure the testing works and delivers results.

Comar is a full-service supplier for diagnostic companies, offering the following value to your operations.

Contact us today to learn more about our high-impact packaging and medical solutions.